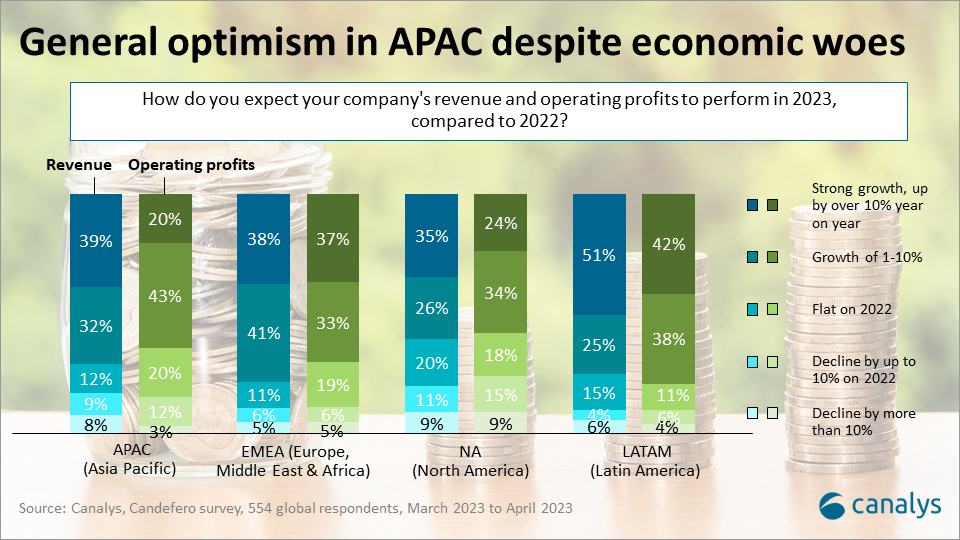

APAC channel optimistic as Canalys Forums 2023 gather pace

7 June 2023

India’s basic watch market has experienced extraordinary growth, driven by consumers’ huge appetite for affordable technology and vendors’ aggressive pricing strategies. But Canalys warns that vendors must differentiate their brands and models, push technological boundaries, focus on creating useful consumer technologies and be aware of the environmental impact of short product lifecycles to sustain their businesses in the long term.

Indian consumers’ huge appetite for affordable technology plus the aggressive optimism of local vendors, such as boAt, Noise and Fire-Boltt, has given rise to the extraordinary growth of India’s basic watch market. The total wearable band market (which includes basic bands, basic watches and smartwatches) in India grew 122% in Q1 2023, solely driven by the basic watch category. Our latest research provided an opportunity to deep dive into the opportunities and risks for the wearable band market in India. In the context of the global wearable band market’s performance, Canalys defines the majority of watches available in India as “basic watches” as they do not come with fully fledged operating systems supported by first- and third-party apps.

The strong demand for basic watches that has developed in India is not organic. Vendors timed the category launch well two to three years ago, with growth fueled by the pandemic as consumers became more health-conscious, buoyed by aggressive pricing strategies. But the lack of core, strong use cases is worrying, and ignoring this means future failure.

Continued strong growth of basic watches expected

Based on an already scaled down “basic” OS, Indian wearable vendors have downplayed the focus on health and fitness to achieve lower price points. This has led to extraordinary new market growth in a short time. The selling points of wearable bands has shifted dramatically in India to make them trendy fashion items. Vendors are chasing this narrative as they aim to continue increasing penetration, by boosting local production and lowering prices from INR2,000 (US$24) to an incredible INR1,000 (US$12).

Local Indian vendors believe that:

As fashion items at extremely low prices, vendors are seeing watch lifecycles as short as six months, in line with the global fitness band market in the early years. These devices had lackluster tracking performance leading to high abandonment. But Indian vendors believe users will continue to look for new devices from a large variety provided by all brands, and the short lifecycle is being seen as an opportunity instead of a threat. Such optimism is admirable, and necessary for companies that are start-ups and VC-funded.

Yet despite this optimism, Canalys believes that to create long-term market success vendors must:

New players try to differentiate from their predecessors

The wearable band players in India stand out when compared with the first batch of homegrown smart device companies, such as Micromax, Lava, Intex and Karbonn. The newer breed of technology companies put more focus on marketing and branding while ensuring margins by shifting to local manufacturing.

Local wearable players are also taking the right steps by:

Diversification to sell accessories puts boAt, Noise, Fire-Boltt and others at risk of becoming lifestyle brands rather than technology brands. But emerging wearable brands still risk ending up like their predecessors, unable to change the market perception of selling low-end devices of inferior quality. Those vendors that continue to take the easy path with the strategy of flooding the market with a lot of models with little consistency in quality and user experiences will eventually pay the price. Most vendors hope to identify “hero models” while they continue to ride the wave. But waves recede fast, as do fashion trends. Canalys expects logic will return to buying behavior, with consumers soon seeking the real value of wearing watches. Failure to deliver value in health and tracking and smart software features localized for users in India risks the category declining aggressively in a short period of time, with vendors unable to fund further development to sustain their businesses.

Wearable bands are not essential devices yet

Canalys installed base estimates show that the 2022 penetration of wearable bands among smartphone users in India was 7%. We forecast this will hit 9% in 2023. Believing that penetration in India will reach above 30% is self-deception at best. Canalys has already seen the rise and fall of the wearable band market in China and the US, with a penetration rate expected to top out at around 28% for 2023. Nothing indicates India’s consumers will behave any differently.

While the market leaders cite a strong willingness to invest in R&D, it is yet to be seen if they can really achieve breakthroughs. They have yet to showcase a collection of reliable health and fitness data with good sensors and tracking algorithms. These would need to be combined with the continuous development of sensor components, tracking algorithms and health insights for users to make them essential consumer health devices.

A time to take charge of their own futures

Now is the time for Indian vendors to build on their success or face being left behind. They are in danger of underestimating consumers, who are hungry for new and exciting technologies. The global wearable band market is also no stranger to new players entering the market, as well as plenty of failures and exits by once-promising players, such as Pebble, Microsoft and Nike. How long can Indian companies ride the wave before realizing it’s time to hope for the best but prepare for the worst?