Digitalization leverages healthcare and active lifestyle awareness

9 May 2022

In the last three years, automotive has become an important strategic market for Qualcomm. It has transformed its product and solutions portfolio, made acquisitions and investments, and grown its customer base and order pipeline.

Qualcomm sold its first telematics solution in 2002 and launched its first infotainment chipset in 2014. It slowly built an automotive solutions portfolio, and customer list, over more than 15 years, but automotive was still a tiny part of its total QCT (Qualcomm CDMA Technologies) business. Automotive was not a major strategic area for Qualcomm. Automotive updates were typically kept until the end of presentations, at CES 2017, for example, VR and drone announcements preceded the automotive update in the Qualcomm keynote. In 2018, after two years of trying, it pulled out of the planned acquisition of auto chip supplier NXP Semiconductors. It was a costly failure, but was likely the trigger for Qualcomm to take control of its destiny in automotive, and really chase broader digital cockpit, autonomous driving and software defined vehicle opportunities.

With 5G now established, Qualcomm is keenly pursuing the huge growth opportunities in automotive, and other sectors. It is leveraging its position in connectivity to pursue a one-stop-shop approach for automotive OEMs and tier one suppliers. Its solutions have evolved from the Snapdragon 602A in 2014, with development, and design wins accelerating with the 3rd and 4th generation Snapdragon Automotive Cockpit Platforms, announced in 2019 and 2021 respectively. It has moved from being a provider of infotainment and telematics solutions, to offering integrated, scalable, customizable, cloud-connected automotive solutions and in a digital platform with the Snapdragon Digital Chassis, announced in 2021.

Qualcomm’s President and CEO, Cristiano Amon has been a very visible supporter of its automotive push, keynoting at several automotive and technology industry events in the past year. In a recent presentation he said, “Car companies are becoming tech companies, and vehicles are going to be connected 100% of the time. The Snapdragon Digital Chassis is our platform for the future of automotive, We have an incredible opportunity to scale very fast”. Qualcomm is increasing its automotive R&D with a new engineering software office in Berlin to increase support of automotive partners in Europe. But the acquisition of Veoneer’s ADAS software unit Arriver, that closed in April 2022, is the big indicator of Qualcomm’s ambitions in automotive. Automotive tier one supplier Magna had agreed a definitive agreement to acquire Veoneer in July 2021, but within weeks Qualcomm had offered substantially more to secure the deal. In doing so, it added crucial ADAS, and collaborative and autonomous driving assets to its automotive solutions portfolio, specifically to the Snapdragon Ride Platform.

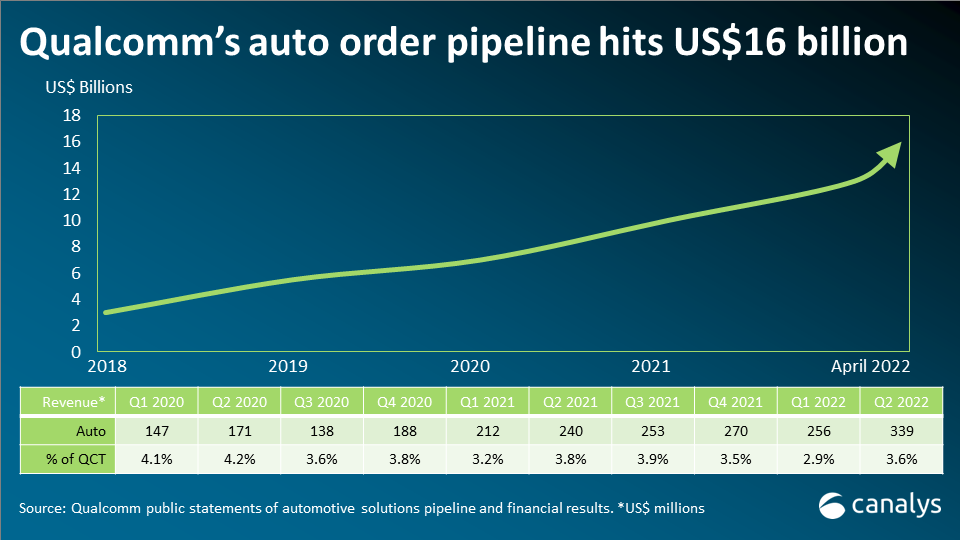

Qualcomm has more than 25 automotive OEMs and many tier one suppliers and solutions providers as strategic partners. However, more recent wins, including multi-year technology collaborations, put it in a much stronger position. In his CES 2022 presentation Cristiano Amon said Qualcomm was applying “the same recipe” that worked so successfully for the company in smartphones – an ominous situation for incumbent suppliers in automotive. In its latest financial results it announced it had an order pipeline of US$16 billion for its automotive solutions. By comparison, in 2019 its order pipeline was US$5.5 billion and US$3 billion in 2018. Revenues for automotive products exceeded US$300 million for the first time in fiscal Q2 2022, but remain less than 4% of total QCT revenues.

If automotive OEMs create their own operating systems: Qualcomm lists Tesla as a customer (connectivity), however, like Apple, Tesla has a closed operating system and a vertical model. Tesla has in-house development of much of its digital cockpit and driver assistance features, its cars have been software defined for more than a decade and it is years ahead of any other car maker regarding OTA updates. Tesla is the only global car maker to grow by every KPI – deliveries, revenue, profit, and keeping vehicle delivery times at manageable levels during the last two years. It currently has two of the top five best selling cars in China and two of the top ten best selling cars in Europe and the US (excluding pick-up trucks) and it will gain more market share in 2022. Tesla’s continued rise is not great news for Qualcomm, but not many OEMs can follow its strategy.

The continued decline in car sales and car ownership: Car sales peaked in 2017 and have been trending down ever since. Alternative ways of getting around were already impacting car ownership. The pandemic then impacted our daily travel routines. Nine month wait times for new cars due to component shortages is not unusual. Rising inflation and living costs have created economic uncertainty and strict lockdowns in Mainland China and the conflict in Ukraine will also impact car sales in 2022. Indeed, car sales declined in all major markets in Q1 2022 – in China sales declined by 9%, sales were down 11% in Europe and were down 16% in the US in Q1. Qualcomm’s automotive OEM customers will face continued challenges, which could delay or jeopardize new feature rollouts.

The full SWOT of Qualcomm’s strategy in automotive is presented as part of a series of digital cockpit ecosystem vendor strategy reports, included in the Canalys Digital Cockpit Analysis service. Alibaba, Baidu, BlackBerry QNX, Google, Huawei, Nvidia and others will also be profiled in 2022.